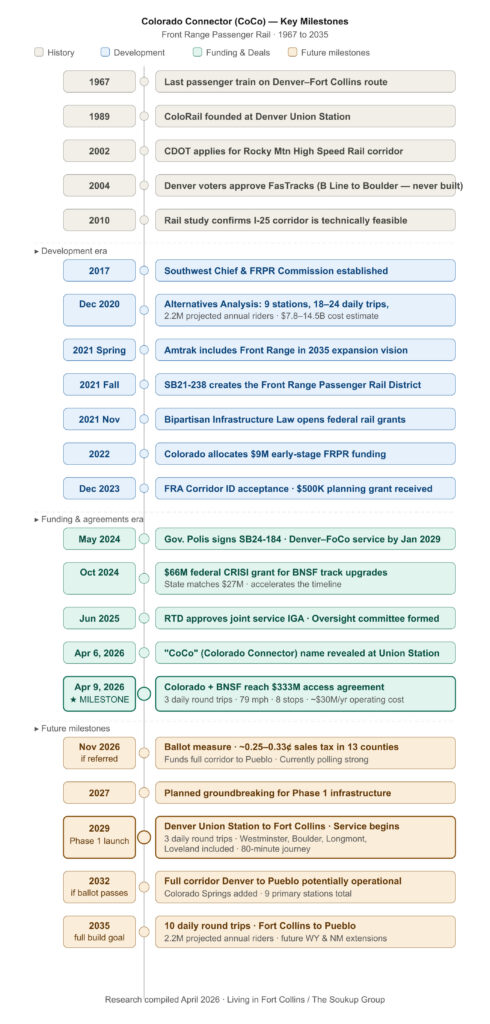

For years, Front Range Passenger Rail felt like one of those ideas Colorado loved to talk about but never quite seemed ready to build. That is starting to change.

Today, the conversation is no longer just about a distant dream of trains running up and down Interstate 25. It is about a defined first phase, identified funding sources, negotiated access to freight rail corridors, and a near-term target to begin starter service between Denver and Fort Collins in 2029. At the same time, the larger vision remains intact: a long-term passenger rail corridor connecting Fort Collins to Pueblo, with future connections discussed beyond Colorado as well.

The big takeaway is this: Colorado may finally be moving from rail planning to actual rail implementation. But the version most likely to happen first is more modest than many people imagine. The first phase is not a full high-frequency regional rail network. It is a starter service designed to prove the concept, build momentum, and create a path toward something much larger.

What Is Front Range Passenger Rail?

Front Range Passenger Rail is the long-discussed plan to create passenger train service along Colorado’s Front Range, linking major population and employment centers such as Fort Collins, Loveland, Longmont, Boulder, Denver, Colorado Springs, and Pueblo. State and district materials frame the project as a way to improve mobility, reduce dependence on I-25, connect communities, and create a stronger transportation backbone for one of the fastest-growing regions in the country.

The current planning structure includes two overlapping efforts. One is the full Front Range corridor vision from Fort Collins to Pueblo. The other is a smaller “Joint Service” or starter phase between Denver Union Station and Fort Collins, which is being advanced first because it is cheaper, more feasible, and more politically achievable in the near term.

What Happens First?

The most likely first phase is a Denver-to-Fort Collins starter line targeted for 2029. Current state materials describe this service as operating with 3 daily round trips, 7 days a week, with stops including Denver, Westminster, Broomfield, Louisville, Boulder, Longmont, Loveland, and Fort Collins. Public documents also describe a target travel time of about 108 minutes end to end, with an 80-minute pure run-time target.

That matters because it brings the project out of the abstract. Instead of asking whether Colorado will ever have passenger rail, the more realistic question now is whether the state and its partners can finalize agreements, complete construction, secure operations funding, and hold the political coalition together long enough to get this starter line running by 2029.

What Comes After the First Phase?

The larger long-term vision is much bigger than the 2029 starter line. Current planning materials support a full Fort Collins-to-Pueblo corridor, with nine major station markets and a service concept centered around 10 daily round trips by 2035. Official presentations describe the long-term strategy as using existing infrastructure where possible while building toward a more robust corridor over time.

In other words, the first phase is not the final product. It is the entry point. If the Denver–Fort Collins service performs well, proves demand, and maintains political support, it could become the foundation for a true Front Range rail system that extends farther south and operates much more frequently.

How Many Trips Could Riders Expect?

For the starter phase, current public materials point to 3 round trips per day. That means six one-way trips daily across the corridor. This is enough to establish service and give people another option besides driving, but it is not yet frequent enough to function like a true all-day, turn-up-and-go rail network.

For the longer-term buildout, the recommended alternative being advanced through planning is 10 round trips per day across the larger corridor. That would represent a major jump in usefulness, flexibility, and daily relevance for commuters, regional travelers, students, and people making occasional business or recreational trips.

How Many People Could Be on Each Train?

For the first phase, the clearest public number is capacity. State materials say the initial trainset could be around 5 cars with roughly 200 seats per train. With 3 round trips per day, that translates to around 1,200 seats offered daily and roughly 445,000 passenger seats annually.

For the long-term recommended corridor alternative, planning materials estimate about 990,000 annual riders under the 10-round-trip scenario. Spread across 20 one-way trains per day over the course of a year, that works out to an average of roughly 136 riders per one-way trip. That is an inferred average based on published annual ridership, not a guaranteed train-by-train number, but it gives a useful sense of scale.

How Is the First Phase Supposed to Be Funded?

One reason the 2029 starter phase has gained momentum is that backers are not relying entirely on a brand-new tax just to get the first trains moving. Current state materials say the initial phase can be advanced through a mix of existing and recently created revenue streams, including SB24-184’s rental-car congestion impact fee, SB24-230’s oil-and-gas-related Clean Transit Enterprise revenue set-aside, RTD participation, and future farebox and ancillary revenue.

That funding package is a major shift in the conversation. It means supporters can plausibly argue that Colorado has a path to launch starter service without immediately asking voters for a new dedicated sales tax just for phase one. That makes the first step politically easier, even if larger future phases will almost certainly require more substantial public funding.

How Could It Be Funded Moving Forward?

Long term, the funding challenge gets much bigger.

The starter phase is measured in the hundreds of millions. The broader corridor is measured in the billions. Colorado’s state rail plan cites earlier estimates of roughly $3 billion to $3.5 billion for a smaller multi-trip system, and older visioning work was even more expensive depending on speed, frequency, and infrastructure assumptions.

That means the long-term funding stack will likely need to include several layers: continued state fee revenue, federal rail grants, local and regional partner contributions, and eventually some form of voter-approved tax or districtwide dedicated revenue. The Front Range Passenger Rail District was created in part to give the project a formal entity capable of planning, financing, and advancing that larger system.

Federal support is especially important here. Colorado entered the Federal Railroad Administration’s Corridor Identification and Development Program, which helps position projects for future federal investment and major grant opportunities. The state has also already won a $66.4 million CRISI grant tied to corridor improvements that support future passenger rail readiness in the northwest part of the Front Range.

How Are They Actually Doing This?

Perhaps the most important evolution in the project is strategic. Earlier visions leaned more heavily toward faster, more expensive rail concepts. The current approach is more incremental and more practical: use existing rail corridors where possible, negotiate with freight railroads, phase the service in, and build something financially plausible before trying to build something idealized.

That is why the BNSF-related progress matters so much. A rail project like this lives or dies not only on public enthusiasm, but on whether the state can secure track access, define capital improvements, and create an operational framework that freight partners will actually accept. Recent commission materials suggest that Colorado has made meaningful progress on exactly that front for the Denver–Fort Collins starter service.

What Are Supporters Saying?

Supporters argue that Colorado cannot keep widening highways forever and expect that alone to solve Front Range mobility problems. They say population growth, increased congestion, and rising travel demand make it necessary to build a more diversified transportation system. In that framing, passenger rail is not a luxury. It is overdue infrastructure for a region that continues to add people, jobs, and travel demand along a narrow north-south spine.

Proponents also point to broader benefits beyond transportation. They argue that rail can improve access to jobs, higher education, health care, entertainment, and recreation while supporting redevelopment around stations, reducing crash exposure, and lowering long-run dependence on highway expansion alone. State materials also cite strong public support in polling and outreach.

What Are Critics Saying?

Critics tend to raise several recurring concerns.

The first is cost. Even if the starter phase is relatively modest compared with earlier concepts, the long-term buildout still requires significant capital and ongoing operating support. Skeptics worry that Colorado could start something that becomes more expensive over time or requires larger subsidies than supporters currently emphasize.

The second is usefulness. A starter service with 3 round trips per day is meaningful, but critics can fairly argue that it may not be frequent enough to change travel behavior for a large share of people. If trains are too infrequent, too slow, or not well-integrated with local transit at each end, the service may feel more symbolic than transformative in its early years.

The third is prioritization. Some opponents believe Colorado should focus more on roads, local transit, or other infrastructure needs before pursuing intercity passenger rail. Others support the rail concept in principle but worry that without strong last-mile transit, people may arrive at stations only to face inconvenient local connections. That criticism is especially relevant in a region where many destinations remain car-oriented.

What Could the Economic Impact Be?

The economic case for Front Range Passenger Rail is one of the strongest arguments supporters have, but it should be discussed honestly.

Colorado’s 2024 state rail plan cites earlier Amtrak corridor analysis estimating more than $103 million in annual economic impact and about $4.3 billion in economic activity generated by initial capital investments. Those are meaningful numbers, but they come from broader corridor visioning rather than a final benefit-cost study for the exact current phase plan now being advanced.

Still, the direction of impact is not hard to understand. Construction spending alone would be significant. Beyond that, rail can expand labor-market access, connect housing markets to employment centers more efficiently, support station-area redevelopment, increase visitor spending, and reduce some of the friction that currently comes with Front Range travel. Even when the exact future impact is debated, the categories of likely benefit are fairly consistent.

How Could This Impact Housing Along the Front Range?

This is where the rail conversation becomes especially important for real estate.

If Front Range Passenger Rail becomes real, it could gradually change how buyers, renters, developers, and employers think about geography. Places that currently feel a little too far from a job center may begin to feel more connected if reliable rail service reduces the mental and practical burden of driving. That does not mean rail instantly erases distance, but it can absolutely compress perceived distance.

For housing, that could show up in several ways.

First, station-area locations could become more valuable over time. Homes, apartments, and mixed-use projects near stations in places like Fort Collins, Loveland, Longmont, Boulder-area connections, and Denver-adjacent nodes may attract additional demand because access to rail becomes part of the value proposition. That is especially true for buyers who want optionality: not necessarily using the train every day, but liking the fact that they can. This is an inference based on the project’s station-oriented service model and the district’s stated emphasis on transit-oriented development and redevelopment around stations.

Second, rail could modestly widen the practical commuter shed along the Front Range. A household that today would rule out living in one city while working in another might begin to reconsider if rail becomes dependable, comfortable, and competitively timed versus driving on I-25. Over time, that could redistribute some housing demand, not necessarily away from Denver or Colorado Springs, but toward communities that gain strong station access and still offer relative affordability or quality-of-life advantages. This is a reasoned inference from the mobility goals and corridor design, rather than a published forecast.

Third, the project could intensify pressure for denser housing near stations. If public leaders want the rail line to succeed, they will likely face growing pressure to allow more housing, more mixed-use development, and better walkability around station areas. Rail tends to work best when people can easily live, work, shop, or connect to local transit near stations. That means zoning and land-use policy may end up mattering almost as much as the trains themselves. This is also an inference, but it follows directly from the project’s economic development and access goals.

Fourth, there could be a split outcome across markets. Communities with stations may see stronger demand and redevelopment pressure, while communities without convenient station access may feel less direct benefit. In other words, rail may not lift all Front Range housing markets equally. The biggest effects are likely to cluster where station access is real, visible, and easy to use.

For Northern Colorado specifically, this could become a bigger deal than many people assume. If Fort Collins and Loveland gain meaningful rail connectivity to Denver and eventually to the larger corridor, that strengthens their positioning for people who want Northern Colorado quality of life while preserving better regional access. That does not automatically lower housing costs. In fact, in some areas it could do the opposite by increasing demand near desirable station-adjacent locations.

The housing takeaway is simple: passenger rail does not just move people. It can reshape how people value place. And when that happens, it can influence prices, development patterns, density debates, and which communities become more competitive in the broader Front Range housing market.

Final Thoughts

Front Range Passenger Rail is still not guaranteed. There are still funding questions, political risks, coordination challenges, and the basic reality that transportation megaprojects are hard. But this project is no longer just a concept sitting on a shelf.

Colorado now has a real starter-phase concept, identified funding sources, advancing agreements, and a clearer path than it has had in years. The likely first version is a 2029 Denver-to-Fort Collins line with 3 daily round trips and roughly 200 seats per train. The larger long-term goal remains a Fort Collins-to-Pueblo corridor with around 10 daily round trips by 2035.

If that happens, the implications go well beyond transportation. This could affect how people commute, where businesses invest, how local governments think about growth, and how housing markets evolve near future station areas across the Front Range. That is why this project matters. It is not just about trains. It is about the future shape of Colorado’s growth.

If you want, I can turn this next into a YouTube script with a strong hook, re-hooks, and a Fort Collins/Northern Colorado angle.